India’s manufacturing sector is expanding at pace, with the market projected to grow from USD 1.63 trillion in 2025 to USD 2.47 trillion by 2031 at a CAGR of 7.26%, per Mordor Intelligence, and private corporate investment announcements reaching ₹14.6 lakh crore in H1 FY 2025–26 alone, per PIB. At this scale, procurement decisions made without structure on vendor familiarity, single quotes, or historical pricing become one of the most significant and least visible drains on project and operational margins.

Procurement strategy consulting in India addresses this gap directly: by bringing structured vendor evaluation, cost benchmarking, and sourcing methodology to decisions that most manufacturers treat as operational routine. When input costs are benchmarked against verified market data, and vendor selection is assessed against technical, financial, and compliance criteria rather than relationships alone, the output is measurable in cost variance recovered, supplier risk avoided, and procurement cycle time reduced.

“IMARC Engineering provides procurement strategy consulting to manufacturers, investors, and EPC/EPCM stakeholders across India. This article sets out the data context, the selection and benchmarking criteria that matter most, and how structured procurement consulting translates into better project and operational outcomes.”

Why Structured Procurement Strategy Matters in India’s Current Industrial Cycle

Several converging forces are raising the cost of unstructured procurement for Indian manufacturers in 2026.

Manufacturing CAPEX Growth Outpacing Procurement Readiness

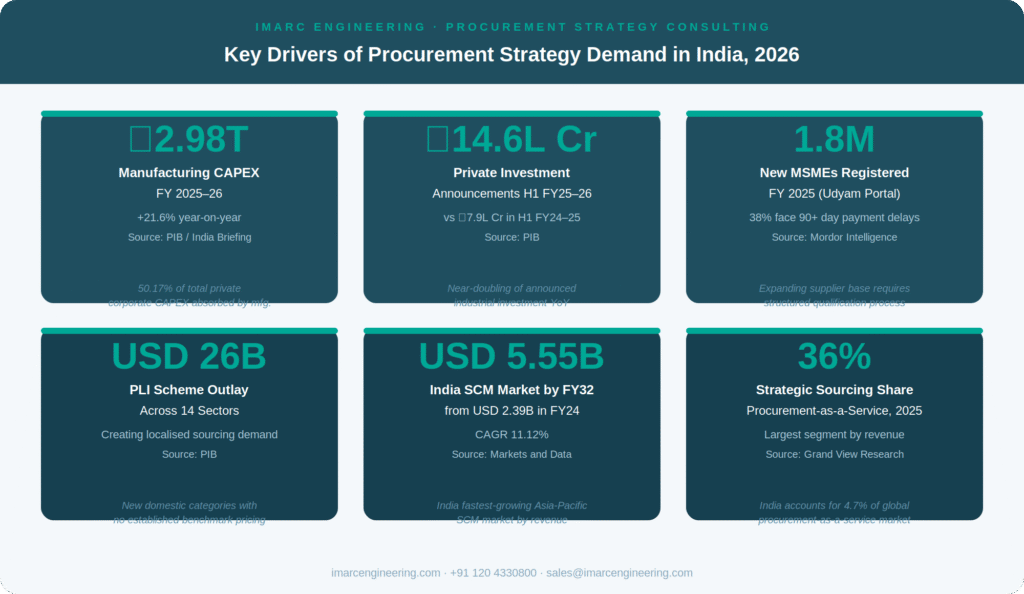

Manufacturing CAPEX reached ₹2.98 trillion (~USD 31.45 billion) in FY 2025–26, up 21.6% year-on-year per PIB and India Briefing, with 50.17% of total private corporate CAPEX absorbed by manufacturing. At this investment velocity, procurement decisions on equipment, raw materials, and services are being made under time pressure rather than with the benefit of competitive market data.

Input Cost Volatility

India’s coal production reached 1,047.52 million tonnes in FY 2024–25, a 4.98% increase per PIB, but domestic production growth has not insulated energy-intensive manufacturers from global input cost cycles. Steel, cement, and chemical producers remain exposed to commodity price movements that compress operating margins when not managed through structured cost benchmarking and long-term supply agreements.

MSME Supplier Base Expansion

Udyam registered 1.8 million new MSMEs in FY 2025 after e-registration was streamlined to two hours, per Mordor Intelligence, expanding India’s domestic supplier base substantially. However, 38% of small manufacturing units still face payment delays exceeding 90 days. A larger vendor pool creates more sourcing options but requires more rigorous evaluation capability, financial stability, and compliance to convert options into reliable supply relationships.

PLI-Linked Supply Chain Localisation

The PLI scheme, with an outlay exceeding USD 26 billion across 14 sectors per PIB, incentivises domestic production but also creates concentrated demand for specific categories of locally sourced components and materials. Manufacturers qualifying under PLI schemes face sourcing constraints in newly localised categories where benchmarking data and qualified vendor lists are not yet established.

Supply Chain Management Market Growth

India’s supply chain management market is projected to reach USD 5.55 billion by FY 2032 at a CAGR of 11.12%, growing from USD 2.39 billion in FY 2024, per Markets and Data. Strategic sourcing was the largest segment of India’s procurement-as-a-service market with a 36% revenue share in 2025, per Grand View Research reflecting the growing recognition that sourcing decisions require structured analytical support, not just vendor relationship management.

These factors place structured procurement strategy ahead of, not after, project award and operations commencement.

Why Unstructured Vendor Selection and Cost Benchmarking Create Margin and Risk Exposure

Most procurement failures in industrial settings are not the result of poor intent. They result from vendor selection based on relationship or prior experience without formal capability assessment, and cost acceptance based on the first or only quote received rather than benchmarked market data.

The categories of risk that surface from unstructured procurement:

- Supplier financial failure mid-contract: A vendor selected without financial health screening delivers late or fails entirely mid-contract, triggering project delays and emergency re-sourcing at premium cost.

- Undetected cost variance: Input prices accepted at 10–20% above market rates on capital equipment, raw materials, or services a variance that is only visible when benchmarked against verified comparable transactions.

- Single-source concentration risk: Single-source supply arrangements for critical materials create vulnerability to supply disruption that a dual- or multi-source strategy would have mitigated.

- Quality non-conformance: Vendors without verified quality certifications (BIS, ISO, or buyer-specific qualification) deliver non-conforming materials that are not detected until construction or production is under way.

- Unscreened ESG and compliance exposure: Procurement decisions made without ESG screening expose buyers to supply chain sustainability risks that affect export eligibility, investor reporting, and customer qualification audits.

Structured procurement strategy consulting replaces each of these exposures with a defined evaluation and verification process applied before supplier engagement is confirmed.

Key Components of Procurement Strategy Consulting for Industrial Manufacturers

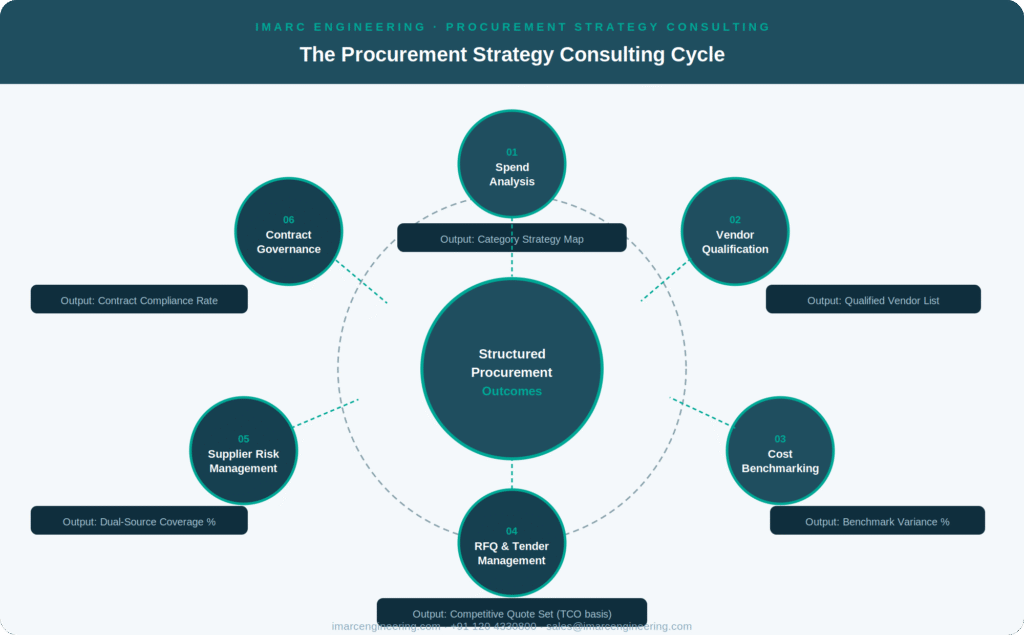

A credible procurement strategy programme addresses six interconnected areas. Each carries its own consequence if left unstructured.

1. Spend Analysis and Category Mapping

- Categorise procurement spend by commodity and category; identify concentration, savings opportunity, and sourcing priority

- Map spend against supply risk and market availability to establish strategy per category partnership, competitive bidding, or spot

2. Vendor Identification and Qualification

- Identify qualified vendors per category through structured market mapping beyond the existing approved vendor list

- Screen against technical capability, quality certification (BIS, ISO), delivery history, and financial health particularly critical for MSME suppliers

- Verify statutory compliance including GST registration, ESI/PF records, and applicable environmental consents

3. Cost Benchmarking and Price Validation

- Benchmark quoted prices against verified market transactions, commodity indices, and DPIIT price data by category

- Develop should-cost models for key categories to support negotiation with a factual, independently verified cost baseline

- Establish re-benchmarking cycles for categories exposed to steel, copper, aluminium, and energy price movement

4. RFQ and Tender Management

- Design RFQ and tender documentation with clear technical specifications, quality requirements, and evaluation criteria

- Evaluate bids on total cost of ownership logistics, quality risk, payment terms, lifecycle cost not quoted unit price alone

5. Supplier Risk Management

- Identify single-source dependencies in critical categories and develop dual- or multi-source strategies

- Monitor supplier performance against KPIs covering delivery, quality, and compliance with ESG screening for export-facing supply chains under EU CBAM and SEBI BRSR

6. Procurement Process and Contract Governance

- Define procurement authority matrices, approval workflows, and contract terms covering escalation, penalties, and dispute resolution

- Implement PO and contract management disciplines ensuring agreed terms are enforced consistently

Procurement Strategy Areas, Unstructured Risk, and Consulting Intervention

The table below maps each procurement area to the risk created by an unstructured approach and the consulting intervention that resolves it.

How IMARC Engineering Delivers Procurement Strategy Consulting

IMARC Engineering structures procurement consulting as an evidence-based process from spend analysis through contract governance replacing informal, relationship-driven sourcing with defined criteria, verified data, and competitive market intelligence.

- Spend analysis and category mapping: Categorising total procurement spend and mapping sourcing strategy by category strategic, competitive, or spot before vendor engagement begins.

- Vendor identification and qualification: Identifying and qualifying vendors against technical capability, quality certification, financial health, and statutory compliance beyond the existing approved vendor list.

- Cost benchmarking and price validation: Benchmarking quoted prices against verified market data and developing should-cost models that support negotiation with a factual cost baseline.

- RFQ and tender management: Designing and running competitive RFQ and tender processes with TCO-based evaluation criteria rather than unit price comparison alone.

- Supplier risk and ESG management: Identifying single-source dependencies and developing multi-source strategies with performance KPI monitoring and ESG screening for export-facing supply chains.

- Procurement governance: Defining authority matrices, contract terms, and PO disciplines that enforce agreed terms consistently across the procurement cycle.

IMARC Engineering supports procurement strategy consulting across chemicals, pharmaceuticals, metals, electronics, food processing, and capital projects sectors where input cost volatility, vendor qualification complexity, and supply chain compliance requirements differ significantly by category and market.

Contact IMARC Engineering’s team for procurement strategy consulting across India.

https://www.imarcengineering.com/contact?service=procurement-strategy-and-cost-benchmarking

Common Mistakes in Industrial Vendor Selection and Cost Benchmarking

- Evaluating bids on unit price rather than total cost of ownership: Awarding to the lowest headline unit price without assessing logistics cost, payment terms, quality risk, and delivery reliability a TCO gap that accumulates across the contract period.

- Not refreshing the vendor pool against market availability: Vendor lists built from prior relationships and never refreshed against India’s expanding MSME supplier base miss lower-cost, higher-quality options that have emerged in localised categories.

- Skipping cost benchmarking for major categories: Input prices accepted without comparison to market benchmarks particularly on steel, copper, and process equipment leave cost variance undetected until a project post-mortem identifies it.

- Selecting vendors without financial due diligence: Approving MSME suppliers without financial health screening creates delivery failure risk that is only discovered mid-contract when remediation options are most limited.

- Treating ESG screening as a reporting formality: Supply chain ESG screening deferred until a customer audit or BRSR submission requires it converts a structured process into a reactive, high-pressure exercise.

Conclusion

India’s manufacturing investment cycle is accelerating, with CAPEX growing 21.6% year-on-year, private investment announcements near-doubling, and 1.8 million new MSME suppliers entering the market in a single year. At this pace, procurement decisions made without structured vendor evaluation, cost benchmarking, and supply risk management directly erode project and operating margins in ways that remain invisible until a post-mortem forces quantification.

Through spend analysis, vendor qualification, cost benchmarking, competitive sourcing, supplier risk management, and procurement governance, IMARC Engineering helps manufacturers and project developers in India convert procurement from a cost centre into a measurable source of competitive advantage.

Contact Us:

IMARC Engineering

Phone: +91-120-433-0800

Email: sales@imarcengineering.com

India: C-130, Sector 2, Noida, Uttar Pradesh 201301

LinkedIn: https://www.linkedin.com/showcase/imarc-engineering/