Introduction

Appointing a distributor is one of the highest-trust decisions a brand makes and one of the most expensive to reverse once credit lines, inventory, and market access have already been assigned. After stock is shipped on credit and sub-dealers are established, hidden financial risks often emerge, such as overextended distributors managing multiple competing brands, informal borrowing that conceals actual debt, or family-run businesses with little separation between personal and company finances.

These risks rarely appear during sales presentations, warehouse visits, or reference checks. They become visible only through a structured distributor financial assessment, which evaluates financial stability, creditworthiness, cash flow, and operational capacity before commercial agreements are signed. By conducting a thorough assessment early, manufacturers can reduce credit risk, protect their investments, and build stronger, more reliable distribution partnerships.

This guide explains how distributor financial assessments work, the financial indicators manufacturers should evaluate before appointing a channel partner, and how structured due diligence helps reduce credit exposure and long-term channel risk.

Why Distributor Financial Health Matters for Channel Partnerships in 2026

India’s expanding credit ecosystem and a large, fragmented distributor base make financial screening more relevant, not less, as brands scale their networks.

Rising Credit Exposure Across the Channel

Total credit exposure to India’s MSME sector, the category most distributors fall into, reached ₹43.3 lakh crore as of September 2025, up 17.8% year-on-year, per CRIF High Mark data. Wider credit access means more distributors are operating with borrowed capital layered onto the trade credit a brand already extends.

Improving but Uneven Asset Quality

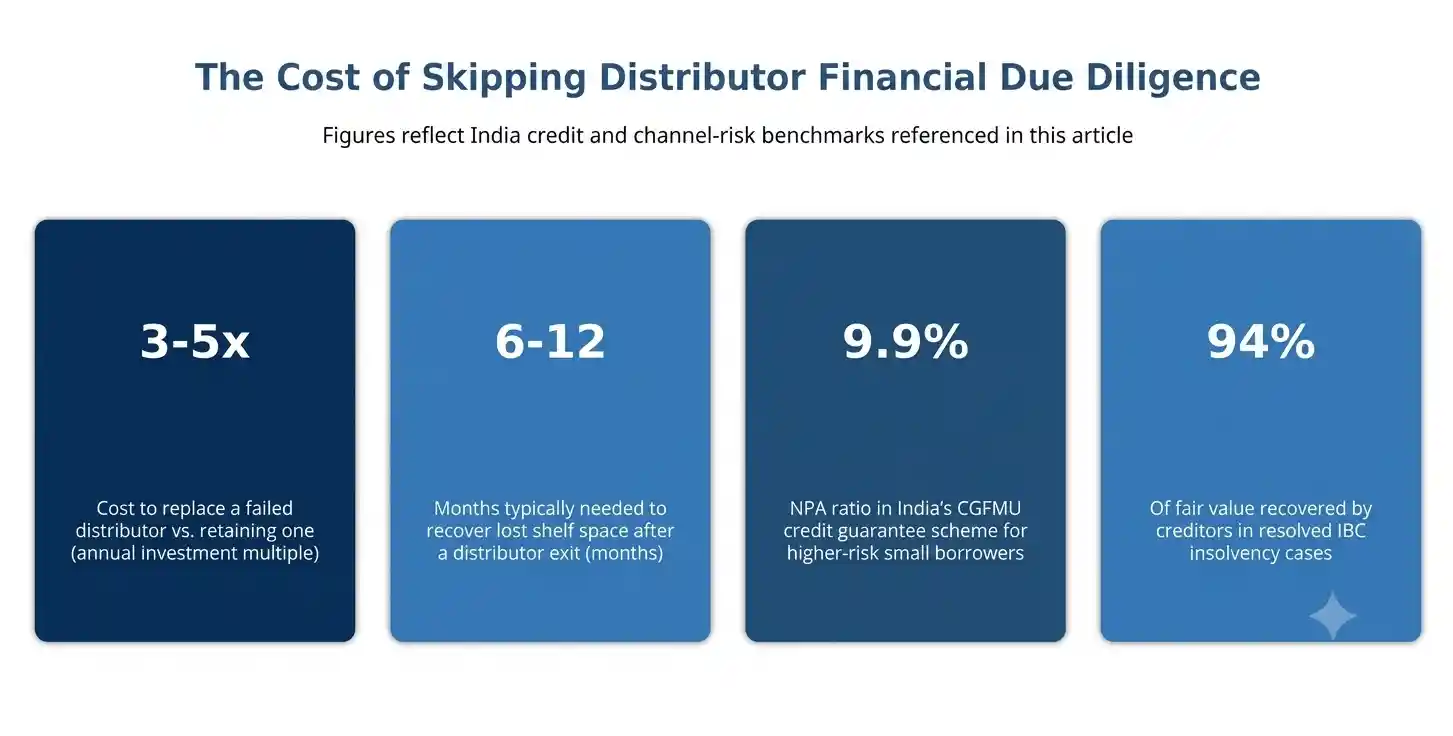

The gross NPA ratio in MSME lending fell from 9.87% in March 2021 to 3.27% as of September 2025, per RBI data a genuine improvement. But within government-backed guarantee schemes covering higher-risk small borrowers, NPA ratios remained at 9.9% under CGFMU and 6.4% under ECLGS as of March 2025, showing that a meaningful share of small distributors still carry real default risk beneath an improving headline number.

A Large, Fast-Formalising Distributor Base

India’s retail distribution runs through roughly 12 million outlets, and large FMCG companies typically manage 40 to 80 distributors each. Registered MSMEs grew from 1.65 crore in April 2023 to 6.5 crore by June 2025, giving brands a much larger base of formally documented partners to verify before signing.

The High Cost of Getting It Wrong

Replacing a failed distributor typically costs 3–5 times the annual investment made in that partner, and lost shelf space can take 6 to 12 months to recover even after a replacement is onboarded. Where insolvency reaches formal resolution, creditors have recovered 94% of fair value on average under India’s Insolvency and Bankruptcy Code a rate only possible when exposure was documented from the start.

Why Weak Distributor Financials Create Channel Risk That Is Difficult to Unwind

Most channel partnership failures follow a predictable pattern: onboarding decided on sales pitch and trade reputation, financial verification skipped or rushed, and commercial pressure to sign before the numbers are checked.

The categories of risk that surface after the wrong distributor is onboarded:

- Credit exposure and bad debt: Extended credit to a stressed distributor often converts into write-offs when the relationship ends abruptly.

- Stock-outs and lost sell-through: Undercapitalised distributors under-order or delay replenishment, creating availability gaps at retail.

- Sub-dealer network collapse: A distributor’s own downstream credit failures can cascade into disputes across an entire territory.

- Shelf space and listing loss: Retailer relationships built by a failing distributor rarely transfer intact to a replacement partner.

- Compliance and GST mismatches: Financial stress often correlates with irregular tax filing, creating audit complications for the brand.

- Continuity and exit risk: A distributor under pressure may exit mid-season, litigate over dues, or be acquired without notice.

Structured financial assessment surfaces these risks or their absence before territory rights and credit terms are committed.

Key Financial Parameters for Distributor Assessment

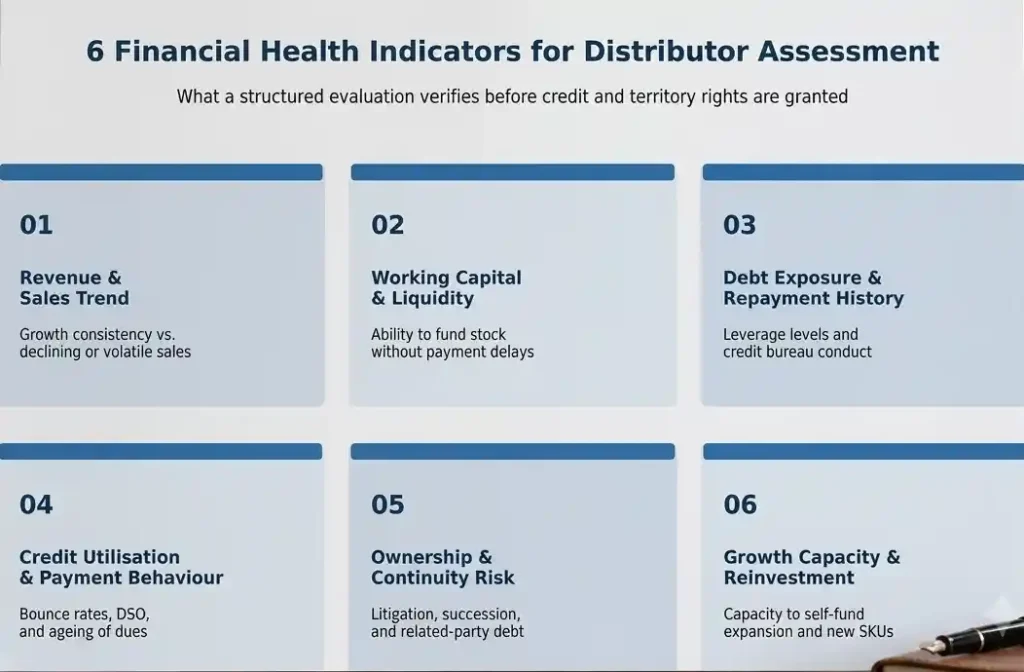

A credible assessment examines six interconnected financial areas. Weakness in any one of them can undermine an otherwise strong-performing distributor.

1. Revenue and Sales Trend

- Growth consistency against category and territory benchmarks

- Dependence on a single brand, principal, or product line

Reported turnover without supporting bank statements or GST returns is a claim, not evidence.

2. Working Capital and Liquidity

- Current ratio, inventory holding days, and cash conversion cycle

- Dependence on the brand’s own credit period to fund operations

3. Debt Exposure and Repayment History

- Total loan exposure across banks and NBFCs

- Credit bureau score and history of overdue or restructured accounts

4. Credit Utilisation and Payment Behaviour

- Cheque and payment bounce rates over the past 12–24 months

- Days sales outstanding against the brand’s stated credit period

5. Ownership Structure and Continuity Risk

- Pending litigation, disputes, or regulatory notices

- Succession plan in owner-managed and family-run businesses

6. Growth Capacity and Reinvestment

- Capacity to self-fund tooling, warehousing, or fleet expansion

- Readiness to support added SKUs or territory without fresh dependence on the brand

How Distributor Financial Assessment Works

A structured assessment replaces trade reputation and sales-pitch confidence with verified financial evidence at every stage.

- Financial documentation review: Bank statements, GST returns, and financials examined for consistency, not just headline turnover.

- Credit bureau and bank reference checks: Independent verification of credit score, repayment history, and exposure across lenders.

- Working capital and liquidity analysis: Assessing whether the distributor can fund stock without depending entirely on the brand’s own credit terms.

- Ownership and litigation screening: Checking for undisclosed disputes, related-party debt, and succession risk.

- Benchmarking against territory peers: Comparing financial strength and credit behaviour across shortlisted candidates.

- Structured reporting: Documented findings supporting credit committee sign-off and periodic re-assessment.

IMARC Engineering provides distributor and channel partner financial assessment services for manufacturers and brands building or scaling distribution networks across India. This article explains what the assessment covers, which financial indicators matter most, and why distributor financial health is a strategic risk decision, not a routine formality.

Speak with IMARC Engineering’s experts to evaluate distributor financial strength and reduce channel partnership risk across India: https://www.imarcengineering.com/contact?service=distribution-partner-identification

Common Mistakes in Distributor Financial Assessment

- Onboarding on trade reputation alone: A well-regarded distributor can still carry undisclosed debt that reputation alone will not reveal.

- Skipping credit bureau checks: Assuming stated turnover reflects real financial health without independently verifying credit behaviour.

- Ignoring related-party and informal debt: Personal guarantees and family borrowing rarely appear in company financials but affect repayment capacity.

- Treating high sales as proof of health: Strong revenue with weak working capital is a common precursor to payment delays and stock-outs.

- No periodic re-assessment: Financial health checked once at onboarding and never reviewed again as exposure grows.

- Relying on informal, verbal credit terms: Undocumented arrangements make it difficult to enforce recovery if the relationship deteriorates.

Conclusion

India’s distribution networks are expanding alongside a fast-growing, increasingly formal MSME credit base, but scale alone does not reduce channel risk it makes financial screening more necessary. Growth in a distributor’s business is sustainable only when backed by verifiable working capital, manageable debt, and disciplined payment behaviour.

Revenue trend, working capital, debt exposure, payment behaviour, ownership continuity, and reinvestment capacity together determine whether a channel partnership holds up under volume growth or unwinds at the first sign of stress. Structured financial assessment replaces assumption with evidence and helps brands extend credit and territory rights with confidence rather than hope.

IMARC Engineering

Distributor Financial Assessment | Channel Partner Due Diligence | Credit Risk Verification | Compliance Checks

Contact Us:

IMARC Engineering

Phone: +91-120-433-0800

Email: sales@imarcengineering.com

India: C-130, Sector 2, Noida, Uttar Pradesh 201301

LinkedIn: https://www.linkedin.com/showcase/imarc-engineering/